In December 2024, when the government announced yet another extension of the Pradhan Mantri Awas Yojana (PMAY), promising homes to every urban family by 2030, the statistics painted a very different picture. Despite a decade of policy announcements, massive budget allocations, and countless speeches about “Housing for All,” the ground reality shows significant challenges that remain unaddressed.

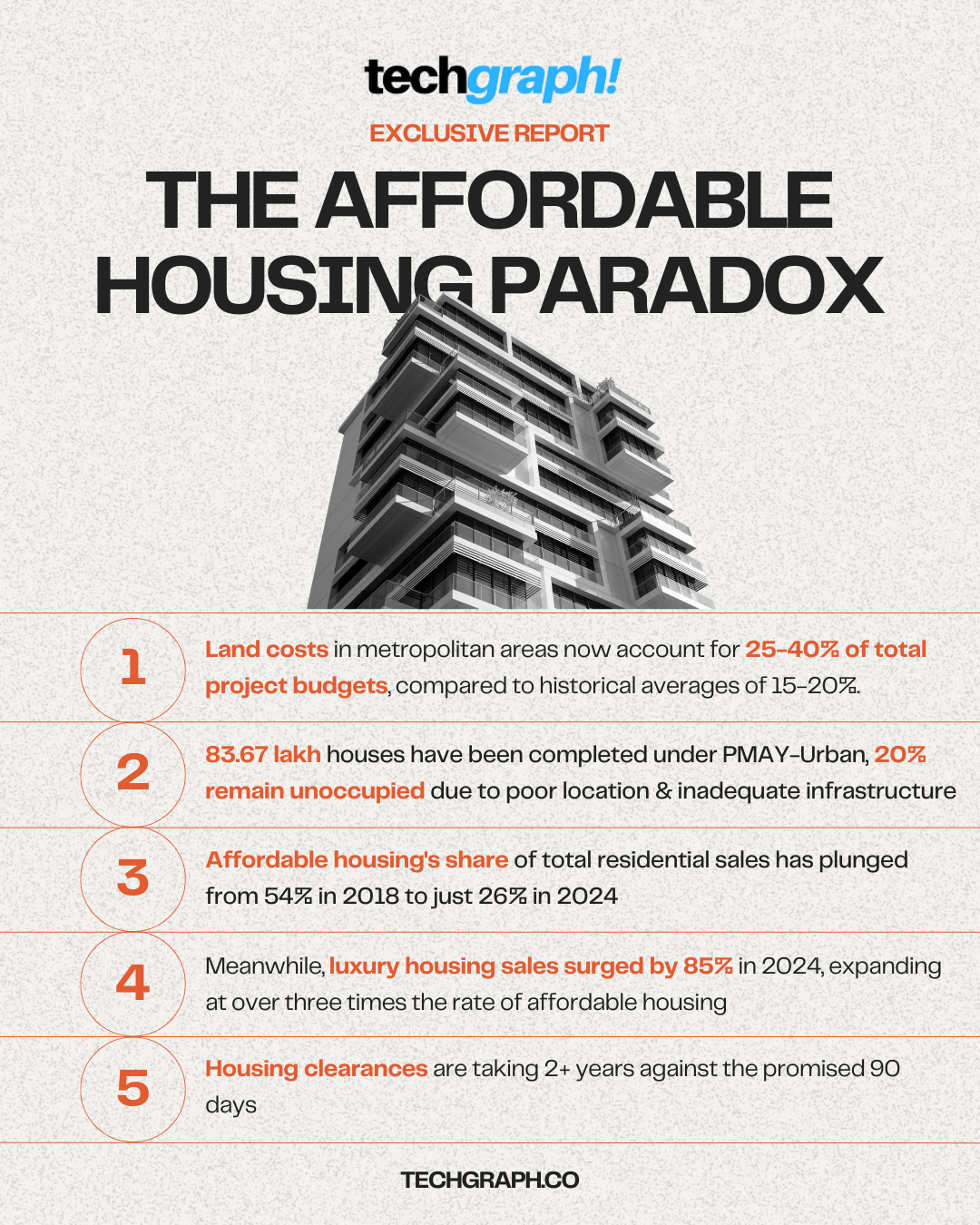

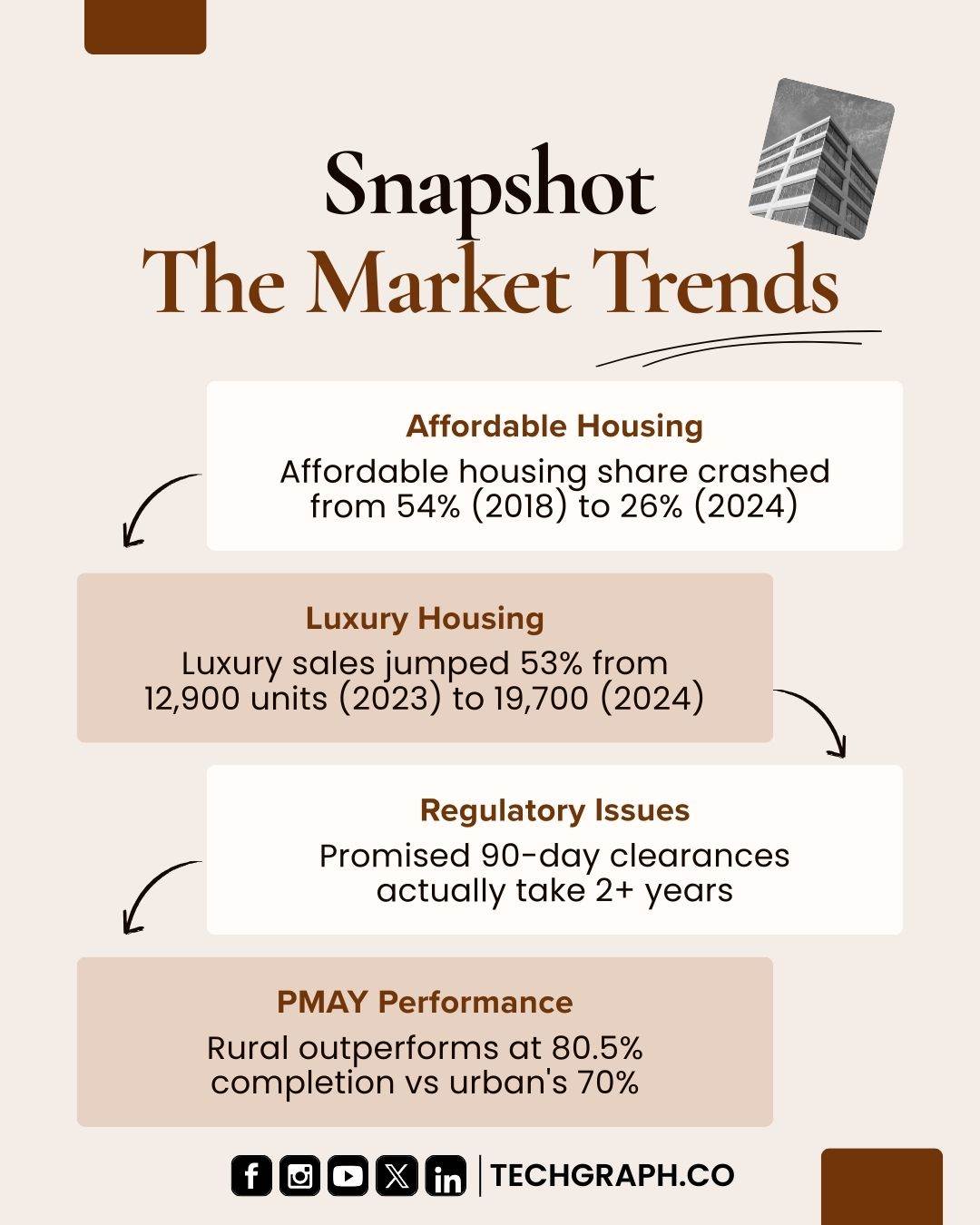

The numbers reveal the scale of the challenge. Affordable housing units have dropped from 54% of total real estate sales in 2018 to just 26% in 2024. During the same period, luxury housing sales have grown substantially, while millions of middle-class families have found themselves priced out. The country now faces a shortage that housing experts project will only get worse if current trends continue.

This investigation, based on government data, industry reports, and extensive interviews with homebuyers, developers, and policymakers, reveals how land speculation, construction cost inflation, regulatory complexities, and lending challenges have made affordable housing increasingly difficult to deliver at scale.

The data shows that about 20% of completed PMAY-Urban houses remain vacant, and a 2023 Parliamentary Committee found that the scheme’s design may not fully serve the landless poor it was intended to help.

The implications go beyond housing policy. When young professionals earning decent salaries cannot afford basic housing in tier-2 cities, when families are trapped in 30-year debt cycles for modest homes, it signals broader challenges in India’s development approach.

Land Costs Have Broken the Basic Math

The most fundamental problem starts with land prices. In Mumbai, average land prices hit Rs 2,16,900 per square meter in 2023. Delhi NCR sits at Rs 98,490 per square meter, while Bengaluru costs Rs 85,035 per square meter. These prices continue climbing by 8-10% annually in prime areas.

The situation isn’t much better in tier 2 cities. Jaipur has seen the steepest surge, with rates jumping from Rs 4,240 to Rs 6,979 per square foot—a 65% increase in just one year. Lucknow and Kanpur now average Rs 6,384 and Rs 6,986 per square foot respectively, while even Dehradun recorded 14% growth.

These rising costs have fundamentally altered project economics. Land acquisition now represents 25-40% of total project costs in metro cities, up from historical norms of 15-20%. For affordable housing projects targeting families earning Rs 3 lakh annually, this makes the basic math impossible. When land alone consumes such a large share of budgets, developers cannot deliver housing at government-mandated price points.

The situation gets worse when you factor in speculative land banking. Real estate companies are acquiring massive tracts, with most deals concentrated around Mumbai and Delhi NCR. This speculation significantly drives up prices above market rates, creating artificial scarcity that pushes affordable housing further into the periphery, where infrastructure is completely inadequate.

Amrita Gupta, Director of Manglam Group, explained the industry’s perspective, saying that rising land costs, regulatory complexities, and inflationary pressures on construction materials often push final prices beyond the intended affordable bracket. She added that it remains important to recognize the significant steps governments have taken, from credit-linked subsidies to policy incentives aimed at supporting affordable housing development.

The government approach to land costs has focused on providing subsidized land through schemes like PMAY. By July 2024, PMAY-Urban had completed 83.67 lakh houses out of 118.9 lakh sanctioned projects. While this represents substantial progress, implementation challenges persist. Many completed units remain unoccupied because projects end up in locations with poor connectivity and insufficient infrastructure.

Construction Costs Have Triggered a Quality Crisis

The construction cost crisis has been building for years, but 2025 data shows how it has fundamentally changed project economics. Construction costs now run Rs 1,700-2,500 per square foot, depending on quality and location.

Here’s what builders are actually paying: cement averages Rs 360-400 per 50kg bag across regions. Steel prices have moderated from their peaks but remain significant. Labor costs have surged to Rs 800-1,200 per day for skilled workers, while materials now comprise about 65% of total project expenses.

These increases have created a devastating quality-price spiral in affordable housing. To meet government price caps, developers have had to compromise on materials and specifications. Projects now routinely use lower-grade cement, reduce steel reinforcement in non-critical areas, and opt for basic construction standards.

What this means is housing that may be nominally affordable but fails to deliver long-term value. Industry reports show that many affordable housing projects experience significant maintenance issues within 3-5 years, ultimately making them more expensive for buyers who must pay for repairs and upgrades.

The Housing Finance Maze Keeps Buyers Trapped

The housing finance sector presents perhaps the most complex challenge for affordable housing. While the market has grown substantially, the reality for middle-class buyers is far more complicated than advertised rates suggest.

Current interest rates range from 7.5% to over 11.50% across different lenders. State Bank of India offers rates from 7.50-8.95%, HDFC Bank ranges from 7.90% upward, and NBFCs charge anywhere from 9.50% to over 11.50%. But these headline rates mask the true cost of borrowing, particularly for first-time buyers in the affordable housing segment.

The experience of Shruti Sharma, a PR executive and homebuyer near Dwarka Expressway, illustrates this perfectly. She was told she’d get an 80% home loan, but the fine print revealed something else. Only 75% was actually covered under the home loan, she said. The rest had to be taken as a personal loan with a higher interest rate. That creates an extra interest burden that was never part of the original pitch.

Her story isn’t unique. Many lenders advertise 80-85% financing, but later split the loan into two parts: a secured home loan and an unsecured personal loan. This extra layer of borrowing destroys affordability rather than enabling it.

Documentation rules create another massive barrier. Most lenders require two to three years of income tax returns, which excludes large parts of the gig economy. Even those who qualify face caps from FOIR rules that limit EMI to 40-60% of income. A family earning Rs 3 lakh annually can only afford EMIs of Rs 10,000-15,000 per month. That limits them to loans of Rs 15-20 lakh. In most cities, that doesn’t buy much of anything.

Government Schemes Deliver Mixed Results with Massive Gaps

The Pradhan Mantri Awas Yojana represents India’s most ambitious affordable housing initiative, with PMAY-U 2.0 promising massive investment for urban families over five years. The rural program has performed significantly better, with 2.69 crore houses completed out of 3.34 crore sanctioned, achieving an 80.5% completion rate.

But urban performance tells a completely different story. Despite substantial budget allocations, urban completions lag significantly. More troubling is that 20% of completed PMAY-Urban houses remain unoccupied, primarily due to incomplete infrastructure, poor location choices, and beneficiary unwillingness to move to peripheral areas.

The Credit Linked Subsidy Scheme (CLSS) has been even more problematic. Originally offering substantial interest subsidies for different income categories, the scheme was discontinued for most categories by March 2022. Processing delays plagued the system, with beneficiaries routinely waiting 6-12 months for subsidy disbursements, defeating the purpose of making housing more affordable.

State-level variations add another layer of complexity. While Gujarat, Tamil Nadu, and Uttar Pradesh show completion rates above 80%, states like Andhra Pradesh, Bihar, and Meghalaya remain below 50%. This patchwork performance reflects inconsistent implementation capacity and political commitment across states.

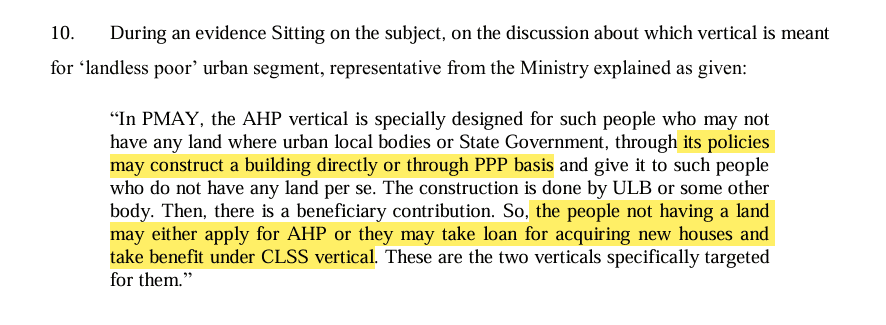

But tthe most damning critique came from the Parliamentary Standing Committee on Housing itself. The committee found that the Beneficiary-Led Construction (BLC) component, which delivers the largest share of PMAY-Urban houses, excludes the landless poor because it requires applicants to own land. During evidence sessions, ministry representatives admitted that states tend to allocate these homes to those who already have land. They explained that families without land can only apply under the Affordable Housing in Partnership vertical, where government bodies build homes directly, or the Credit Linked Subsidy Scheme, which offers loan subsidies. These two routes together account for a much smaller portion of the scheme, leaving the true landless poor with limited options.

Regulatory Approvals Have Become a Nightmare

Perhaps no single factor undermines affordable housing more than regulatory delays. The government promises single-window clearance within 90 days, but industry data shows the reality is over two years, including lengthy waits followed by extended clearance processes.

The approval maze includes environmental clearances, land acquisition approvals, construction permits, fire safety certificates, utility connections, and RERA registration. Each requires separate departments and documentation. Anita Arjundas, MD of Mahindra Lifespaces, described the industry’s frustration, saying that the housing sector expects single window clearance within 90 days, but it has been taking not less than two years, including a six-month wait and later one more year for clearance.

RERA implementation has improved transparency but increased compliance costs significantly. Developers must now maintain 70% of project funds in escrow accounts, file quarterly progress reports, and undergo annual audits. While these measures protect buyers, they add administrative burdens that particularly affect smaller developers who might otherwise focus on affordable housing.

The regulatory burden varies dramatically across states. Maharashtra’s ready reckoner rates affect project viability differently than Karnataka’s 15% affordable housing allocation requirement for projects above 40 acres. Gujarat’s 20% inclusionary zoning requirement creates yet another variation, making it impossible for developers to standardize approaches across markets.

Construction bans add another layer of uncertainty. Delhi NCR’s regular pollution-related construction bans mean that a one-month ban typically causes 2-3 months of project delays. These delays compound approval times and create penalty risks under RERA, further discouraging developer participation.

Developer Economics Have Broken the Affordable Housing Model

The combination of high land costs, construction inflation, financing challenges, and regulatory delays has fundamentally broken the economics of affordable housing development. Private sector participation has declined dramatically, with affordable housing receiving $3.2 billion in investment from 2011 to 2023. While substantial, this still represents a tiny fraction of overall real estate investment.

Project margins in affordable housing typically run 8-12%, compared to 20-25% in premium housing. When land costs consume 25-40% of project budgets and construction costs rise consistently, these thin margins become completely unsustainable. The result is that established developers increasingly avoid affordable housing entirely, leaving the sector to smaller players who often lack the financial capacity to deliver at scale.

The situation is particularly acute in metro cities where land costs make it impossible to deliver housing at government-mandated price points. In Mumbai, average housing unit prices have risen dramatically, pricing out the target demographic entirely.

Recent housing scheme launches illustrate both the demand and the supply constraints. These schemes receive applications far exceeding available units, but even these “affordable” homes are priced beyond the reach of many families. The success factors like government land availability and transit connectivity are rarely replicated in private sector projects.

Infrastructure Deficits Compound the Affordability Crisis

Even when affordable housing gets built, infrastructure deficits undermine its viability completely. The fact that 20% of completed PMAY-Urban houses remain unoccupied reflects deeper problems with location choices and infrastructure support. Projects are often pushed to peripheral locations where land is cheaper, but connectivity, water supply, sewerage, and social infrastructure are completely inadequate.

The government’s Smart Cities Mission covers 100 cities, and AMRUT 2.0 targets 500 cities for water security, but the pace of infrastructure development lags far behind housing construction. This creates a timing mismatch where families receive housing allocations but cannot practically occupy them due to lack of basic amenities.

Urban infrastructure funding provides substantial amounts annually for tier-2 and tier-3 cities, but this investment pales against the infrastructure needs of rapid urbanization. India’s urban population is expected to reach 40% by 2030, requiring massive infrastructure investments that current funding levels simply cannot support.

The Hidden Costs of Housing Finance Reveal Systematic Problems

The housing finance sector’s complexity deserves deeper examination because it reveals how affordability promises often prove completely illusory. While banks and NBFCs advertise competitive rates, the actual borrowing experience involves hidden costs and structural barriers that make housing less affordable, not more.

EMI-to-income ratios provide a stark illustration. For families earning Rs 3 lakh annually, the recommended EMI limit of 40% of gross income translates to Rs 10,000 per month. At current interest rates of 8-9%, this supports loans of Rs 12-15 lakh maximum. But affordable housing in major cities routinely costs Rs 25-40 lakh, creating a fundamental mismatch between what people can afford and what housing actually costs.

The documentation requirements exclude massive segments of the workforce. The requirement for 2-3 years of ITR filing automatically disqualifies most gig workers, small business owners, and informal sector employees. Even those who qualify face additional hurdles like minimum income thresholds that further restrict access.

CIBIL score requirements add another filter. While credit scores have improved generally, many first-time homebuyers in the affordable housing segment have limited credit history. Banks typically require high scores for optimal terms and often reject applications below certain thresholds. This creates a catch-22 where people who most need affordable housing have the least access to affordable credit.

Government Spending Delivers Questionable Value

The scale of government investment in affordable housing makes the poor results even more troubling. PMAY-U 2.0 promises massive total investment with substantial central assistance over five years. The rural program has already spent enormous amounts in central share with total utilization including state contributions.

But the value delivered raises serious questions. The Parliamentary Standing Committee found that the scheme’s design contradicts its stated objectives of serving the landless poor. Multiple audits have noted ineligible beneficiaries receiving scheme benefits, suggesting weak verification processes.

The average cost per PMAY-Rural house is Rs 1.20 lakh in plains and Rs 1.30 lakh in hills, while urban costs are significantly higher. Given construction cost inflation, these amounts may be insufficient to deliver quality housing, leading to the quality compromises documented in multiple reports.

Employment generation claims sound impressive but lack proper verification. Many of these may be temporary construction jobs rather than sustainable employment, and the opportunity cost of this investment compared to alternative uses of public funds remains completely unexplored.

Market Dynamics Have Shifted Decisively Against Affordability

The broader real estate market has shifted decisively away from affordable housing. Luxury housing sales surged by 85% year-over-year in recent periods, while homes priced above Rs 1.5 crore now command 21% of total market share, up from just 10% a few years ago. This dramatic shift reflects rational developer behavior responding to profit margins, regulatory burden, and market demand patterns.

Market absorption metrics have improved overall, with the Quarters to Sell (QTS) dropping from 9.5 quarters in 2021 to 5.8 quarters in 2024, indicating better liquidity across the real estate sector. But this improvement primarily benefits premium housing segments where inventory moves faster and margins are substantially higher. Affordable housing projects often face much longer sales periods due to location constraints and the financing difficulties their target buyers encounter.

Private equity investment patterns confirm this market trend. International investors allocate much smaller percentages of their India real estate investments to affordable housing compared to commercial and premium residential sectors. This reflects their assessment that affordable housing lacks viable business models under current regulatory structures and cost conditions.

The Reserve Bank of India’s House Price Index showed 3.8% year-over-year increases in the latest available data. This consistent upward trajectory across all housing markets makes homeownership progressively harder for middle-class families, often pushing them toward longer-term financing arrangements that significantly increase their lifetime housing costs.

The Bottom Line

Timmana Gouda D, founder of WhatsLoan, points to the core issues around government policies and land supply. He emphasizes that land must be provided free or at government rates to committed builders, along with rent-to-buy schemes modeled after Singapore’s approach. Singapore’s Housing Development Board successfully used reclaimed and state-owned land to build mass-market flats now housing more than 80 percent of its population, providing an effective model for India to consider.

Similarly, Amrita Gupta added, while the demand and opportunity for affordable housing are real, translating these into results requires pragmatic execution, faster clearances, and sustained incentives to turn affordability from a policy promise into a long-term reality.

Despite these perspectives, persistent challenges around land availability, regulatory delays, financing access, and construction methods mean that affordable housing remains out of reach for millions of Indian families.

What’s required is a fundamental rethinking of how India approaches urban development, land use, and housing provision. Based on current evidence, that transformation is still nowhere on the immediate horizon.

[We have been working on this article for two months, cross-checking that all the data we mention is accurate. If we have missed any data or references, please email us.]